Want to use your weekly planner to get your finances under control? Learn how to track your spending with a weekly planner with this foolproof, 5 minutes a day method!

UPDATED August 9, 2020 – This is the method that I used to track our finances for over 10 years! However, I have recently switched to a Budget Spreadsheet method, so be sure to check that out too!

I manage all of the finances in my household. And I’m pretty darn good at it, if I do say so myself!

In our fourteen years of marriage, my husband has not paid one single bill. He doesn’t even know the names of our utility companies… which, by the way, is the reason why I created this In Case of Emergency Binder… and you should have one, too!

But I don’t mind being the money manager in our house. I like numbers and budgeting. And I find it comforting to know exactly how much money is going in and out of our bank account each day.

I feel empowered taking on this role for my family and YOU can track your spending using a weekly planner too, by implementing the simple strategies that I use.

*This post contains affiliate links, which means if you click a link and make a purchase, I earn a commission at no additional cost to you. See my full disclosure here.

How to Keep Track of Spending Using a Weekly Planner

Step 1: Write down ALL expenses and income

Expenses

The first step in taking control of your personal finances is to know HOW MUCH money you are spending.

Did you spend $50.62 at the grocery store? Write it down.

Did you stop at the gas station to fill up? Write it down.

Did you give your kids $3.00 for lunch money? Write it down.

Did your husband go a little crazy at Academy Sports and buy way too many fishing lures? No, that was just my husband? Write it down.

You get the idea. Write down every purchase, big or small that you make throughout the week. My general rule is that if more than $1.00 leaves my bank account or wallet, then I make a note of it. IE – If I give my kids two quarters to throw into the mall fountain, I DON’T write that down.

Income and Deposits

Keep track of the exact amounts of any deposits into your account also.

Track paychecks, PayPal deposits, credits from merchandise returns, etc. You want to know exactly how much money your are bringing in each month so that you can compare your deposits and your withdrawals.

Step 2: Add it all up

At the end of the month, add up all your expenses. You can separate expenses by category if you want, like “restaurants”, “groceries”, “monthly bills”, etc. I like to keep my monthly bills (mortgage, electricity, insurance, car payment, etc) separate from other expenses that are more variable, like groceries, clothing, car maintenance, etc.

If the word “Yikes!” comes to mind, you’re welcome! You now know that you have room for improvement!

All of those gas station sodas, restaurant lunches, and impulse purchases really add up. And you probably didn’t realize the amount of your hard earned money that you had been spending on things that you don’t really NEED.

Now is also the time to add up all deposits.

This will give you a good picture of your actual income for the month, especially if it fluctuates because of commission-only income, etc.

By the way, if you want some good ideas for ways to make money so that you can increase that deposit amount, then check out this post: 5 Low Stress Ways to Make Money as a Stay-at-Home Mom

Step 3: Compare Income to Expenses

Next it’s time to compare the money coming in versus the money going out.

Subtract the total amount of money spent (bills, entertainment, groceries, etc.) from the total amount of money earned.

If your income is greater than your expenses, good for you! Maybe consider investing some of the excess or setting aside a recurring amount for a “rainy day”.

If your expenses for the month are more than what you brought in, you need to seriously look at where you can cut back.

Is it necessary to eat out for lunch three times a week, or can you pack a healthy (and cheap!) lunch from home?

Do you use all of the channels in your current cable or satellite tv package, or can you switch to a lower priced option?

Do you really need that gym membership that you only use once a week, or can you do a workout from home with fitness DVDs that you can check out for free from the library?

There are a TON of ways to save money, even it it’s only a few dollars a week.

If you purge some of the unnecessary purchases from your spending, the savings will add up. And you’ll be one step closer to Personal Finances perfection!

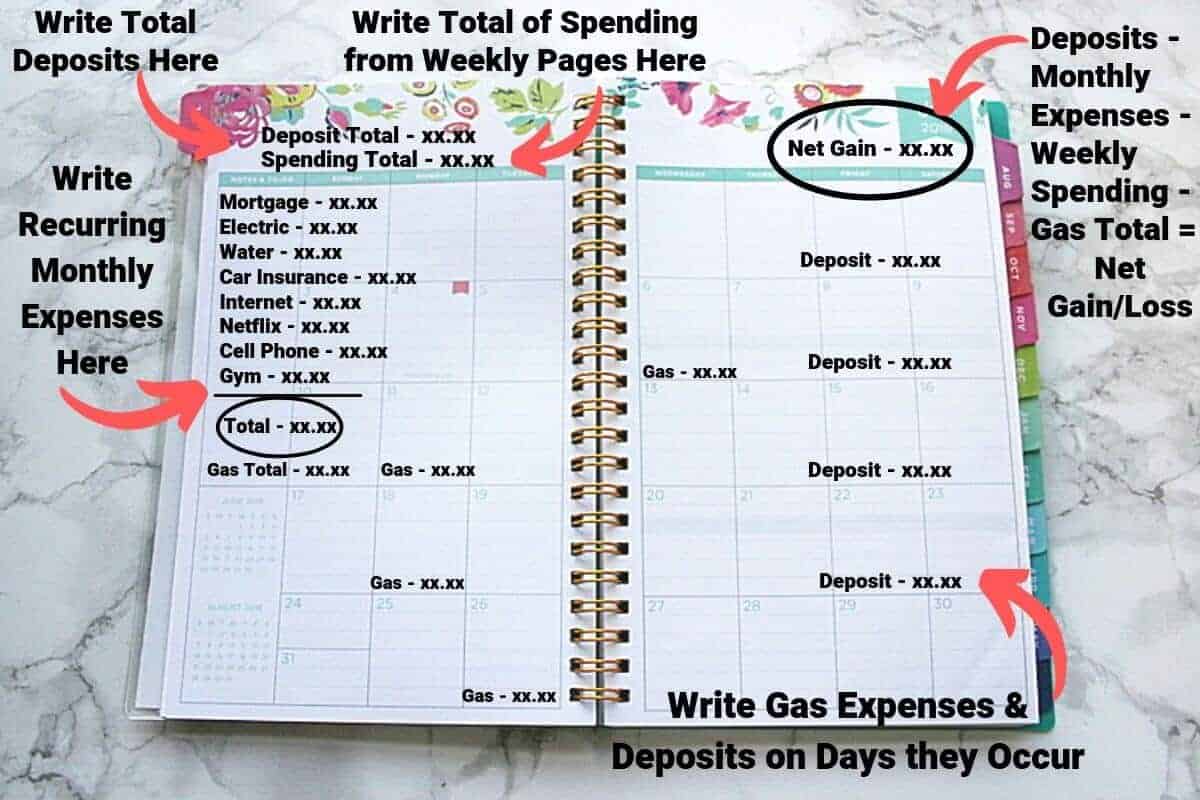

Once you know your net gain or loss (Hopefully gain!) for the month, record that amount somewhere on the month page of your weekly planner. (Check out the graphic below to see where I record my amounts.)

That way, you can easily go back and reference how you did for the month.

Also, at the end of the year go back and add up all of your monthly net amounts to keep track of spending and get a total picture of your financial health for the year.

I give you even more tips for how to track expenses and income in this post, so be sure to check that out!

Where to Write Expenses and Income in Your Planner

First, it’s important to have the RIGHT planner. For my simple method of tracking finances, you will need a weekly planner that has monthly sheets with a lined notes column on one side.

I use a Blue Sky Weekly Planner (affiliate), and I LOVE it! No expensive Personal Finances planner or budget app needed!

On the monthly pages, I document our income for the month along with any recurring payments (car payment, insurance, utilities, etc). Here’s a picture showing you what my monthly planner pages look like:

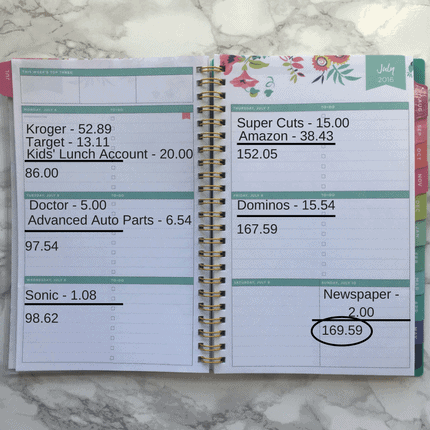

For our other expenses, I use the weekly pages and write down all expenses on the day that they occur. This allows me to keep track of spending each week, and make sure that I’m not going over our weekly budget for variable expenses.

Here is just a sample of how it should look (except not typed – I didn’t want to subject you all to my chicken scratch writing):

And be sure to note EXACT amounts.

On average, my family makes about 30 purchases per week. Rounding up or down on that many transactions could be the difference of $20 per week, or roughly $80 per month.

The Blue Sky Weekly Planner (affiliate) is definitely the best planner that I have come across for this method to keep track of spending. For my needs, it has the perfect amount of space to document all of my transactions. Plus, it comes in all sorts of cute designs. Bonus!

I prefer the 5″x8″ size because I like to keep it in the side pocket of my car door, but it also comes in a 8″ x 11″ as well.

Grab your own Blue Sky Weekly Planner here! (affiliate)

Finding Time to Keep Track of Spending

Don’t have time for that, you say?

Sure you do. If you keep track of spending each day, you won’t be overwhelmed at the end of the week or month.

My TIP – I keep my weekly planner in the side compartment of my car door so it’s nice and handy. And I have the apps for my bank and credit card companies on my phone.

Whenever I have a spare 5 minutes in my car, usually in the pick up line at school, then I check my two apps and write down all of the transactions from the previous day.

Tracking your finances doesn’t have to be difficult or time-consuming, you just need to commit to it!

Once you get in the habit of checking your finances before your Facebook, it becomes much easier to find the time.

Amy @ The Savvy Sparrow

And, if you check your account balances each day, you are much more likely to catch errors made by your financial institutions. They make mistakes, too!

In fact, just last spring I discovered that my bank had withdrawn the funds for my daughter’s preschool payment twice. That was an extra $320 that was taken out of my account. I called the bank and was able to tell them the exact day and amount of the mistake and they credited my account.

If I hadn’t kept such a close eye on my finances, then I could have missed that erroneous charge, so it pays to keep track of your spending!

It Doesn’t Have to Be Difficult to Keep Track of Spending!

This is the EXACT and SIMPLE method that I use to keep track of my personal finances.

I know exactly what we can and can’t afford because I keep track of spending and always have a thorough picture of our financial health. And you can too!

Don’t get trapped in the vicious cycle of spending money over and over again without knowing that you’re actually spending more than you make.

As the saying goes, “Knowledge is Power”. So take the few extra minutes each day to KNOW where your money is going, and have the POWER to make more informed financial decisions!

And be sure to visit this post from Nerd Wallet for even more ideas for tracking your monthly expenses.

If you want to save this method to keep track of spending for later, or want to share it with a friend, please PIN! And thanks for stopping by!

You are truly AMAZING! All of my “where to begin” questions have been answered. Thank you for sharing your insights and examples. Now off to click the link to order a Blue Sky weekly planner and begin my budgeting journey!

I love this idea! Never thought of using it in a planner!

Hi Cati! Yes, this is a GREAT way to track your personal expenses and spending… I especially like that it’s “portable” because I can fill in my expenses when I’m sitting in the car waiting on my kids to get out of school, etc. This method worked for me for years, before I decided to transition to the spreadsheet for the automatic calculations. 🙂

Great article! A very practical way to track expenses.

Thanks so much Marybelle! Glad you enjoyed the post!

Thank you…thank you…thank you..

You’re so welcome, Annabelle! I’m glad the post helped you! It’s so important to track every penny of your income and expenses, but so few people actually do it. 🙂

Thank you so much. This is just what I’ve been looking for. No fluff straight forward how to budget. I have a question? I that okay to post here or can I email you?

Again thank you so much!

Hi Jacquie! Whichever you prefer is perfectly fine! If you would rather email me directly, you can reach me at [email protected] 🙂

Thanks for sharing this wonderful idea.These are absolutely incredible, .Very helpful! Cheers! X

Thanks so much Sofia! 🙂

Thank’s for this article! It helps me to save more money each week! Now i invest them and with the help of it have extra money! It is so cool!

So glad you liked the post! Thanks for your comment! 🙂

Love this idea. So much more useful and doable than any other system I read about. This is something I can do.

Thank you!!

Hi Terri! Yes, it’s a super easy way to keep track of spending, and it’s been working for me for YEARS! It’s also nice because you can keep the old weekly planners (they don’t take up much space – mine are all in a drawer in my nightstand), and go back and reference past years to see how much money you made a particular month, how high your electricity bill was, etc. Thanks for your comment! 🙂